(Insurtech Guide : Focused on US Geography)

Introduction

Commercial property insurance in the United States is fundamentally a data-driven line of business. Every underwriting decision, pricing calculation, claim evaluation, and risk assessment depends on how well data is captured, structured, and interpreted. For software implementation teams, data architects, and AI practitioners, understanding the core data fields and their business meaning is critical. This guide provides a structured, implementation-ready view of the key data attributes used in commercial property insurance, along with their relevance in underwriting systems, analytics, and AI models.

Key Data Segments/Fields

If you want to watch and listen as a video instead of an article you can watch this video to get the insights of this article.

1.

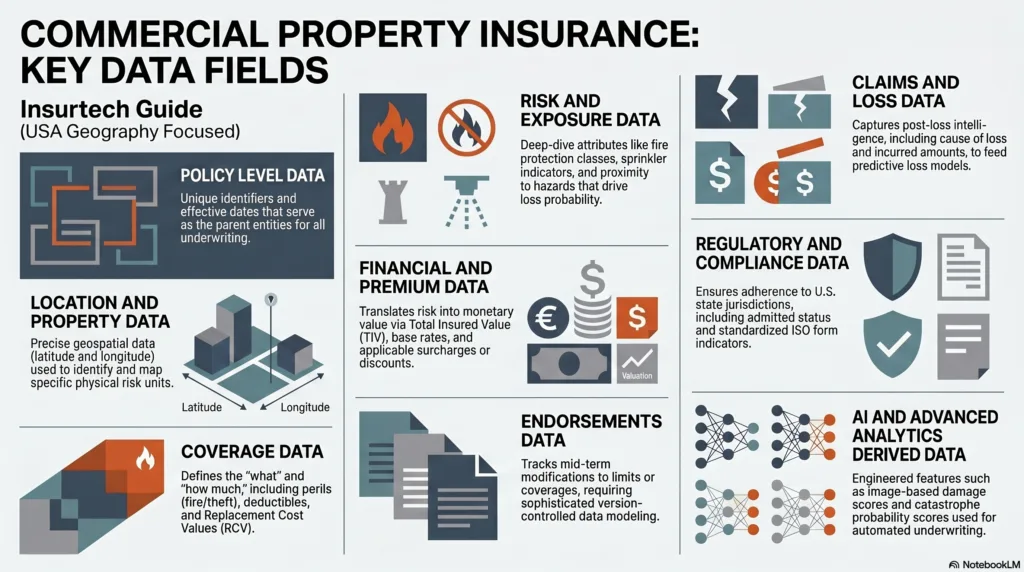

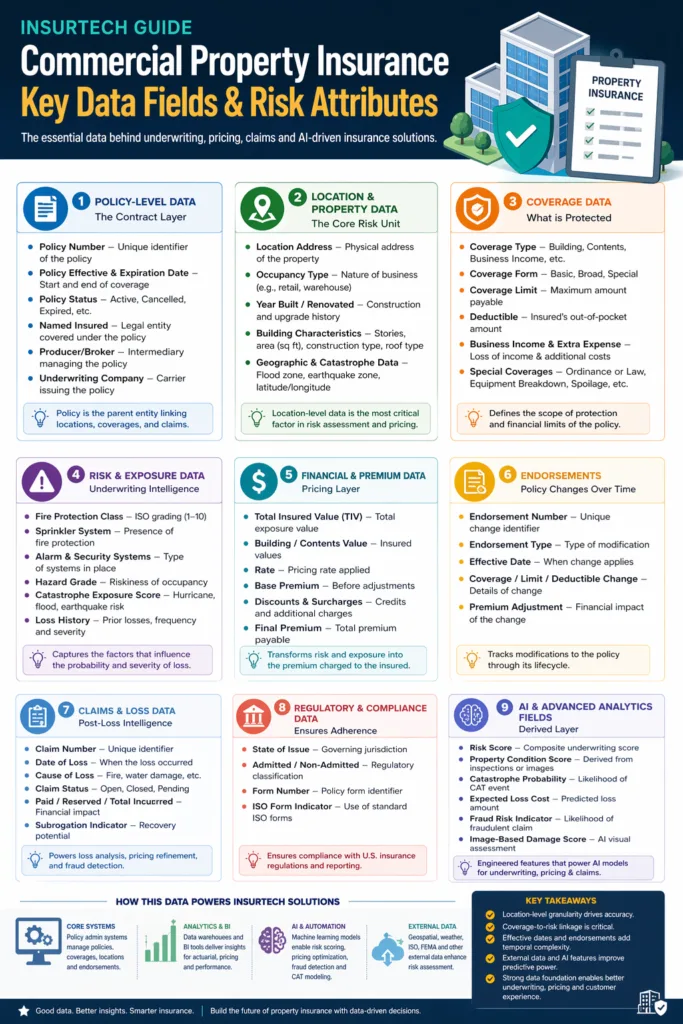

Policy-Level Data (The Contract Layer)

At the highest level, a policy represents the legal contract between the insurer and the insured.

| Data Field ok | Meaning |

| Policy Number | Unique identifier of the insurance contract |

| Policy Effective Date | Start date of coverage |

| Policy Expiration Date | End date of coverage |

| Policy Term | Duration of coverage (typically 12 months) |

| Policy Status | Active, Cancelled, Expired, etc. |

| New/Renewal Indicator | Indicates whether policy is new or renewal |

| Named Insured | Legal entity covered under the policy |

| Additional Insureds | Other entities with coverage rights |

| Producer/Broker | Intermediary managing the policy |

| Underwriting Company | Insurance carrier issuing the policy |

Implementation Insight:

Policy-level data acts as the parent entity in most systems (e.g., Guidewire, Duck Creek), linking all downstream data such as locations, coverages, and claims.

2.. Location & Property Data (The Core Risk Unit)

Commercial property insurance is location-centric. Each insured location represents a distinct risk.

| Data Field | Meaning |

| Location Number | Unique identifier for each insured location |

| Location Address | Physical address of the property |

| City / State / ZIP | Geographic identifiers |

| Latitude / Longitude | Coordinates used for geospatial analysis |

| Building Number | Identifier for multiple buildings at one location |

| Occupancy Type | Type of business activity (e.g., retail, warehouse) |

| Industry Code (NAICS/SIC) | Standard classification of business |

| Year Built | Construction year |

| Year Renovated | Last major upgrade |

| Number of Stories | Total floors |

| Total Area (Sq Ft) | Building size |

| Construction Type | Material (frame, masonry, fire-resistive) |

| Roof Type & Condition | Structural vulnerability indicators |

| Flood Zone | FEMA flood risk classification |

| Earthquake Zone | Seismic risk classification |

Implementation Insight:

This is the most critical dataset for underwriting and pricing. AI models also rely heavily on this layer for risk scoring and catastrophe modeling.

3. Coverage Data (What is Protected)

Coverage defines what risks are insured and to what extent.

| Data Field | Meaning |

| Coverage Type | Building, Contents, Business Income, etc. |

| Coverage Form | Basic, Broad, Special |

| Covered Perils | Fire, theft, wind, etc. |

| Coverage Limit | Maximum payable amount |

| Deductible | Insured’s out-of-pocket amount |

| Replacement Cost Value (RCV) | Cost to replace without depreciation |

| Actual Cash Value (ACV) | Replacement cost minus depreciation |

| Coinsurance Percentage | Required insurance level |

| Blanket Coverage Indicator | Shared limits across locations |

| Business Income Coverage | Loss of income protection |

| Extra Expense Coverage | Additional operating costs |

| Ordinance or Law Coverage | Cost of regulatory compliance |

| Equipment Breakdown | Mechanical/electrical failure coverage |

Implementation Insight:

Coverage data must be tightly linked to locations and buildings, not just policies, to avoid pricing and claims errors.

4.Risk & Exposure Data (Underwriting Intelligence)

This layer captures risk characteristics influencing loss probability.

| Data Field | Meaning |

| Fire Protection Class | ISO grading (1–10) |

| Distance to Fire Station | Impacts response time |

| Distance to Hydrant | Fire suppression capability |

| Sprinkler System Indicator | Presence of fire protection system |

| Alarm System Type | Security/fire alarm details |

| Security Features | CCTV, guards, access control |

| Hazard Grade | Riskiness of occupancy |

| Adjacent Risk Exposure | Nearby hazardous properties |

| Catastrophe Exposure Score | Hurricane, flood, earthquake risk |

| Loss History Indicator | Whether prior losses exist |

| Loss Frequency | Number of past claims |

| Loss Severity | Average claim size |

Implementation Insight:

This dataset is heavily used in rating engines, underwriting rules, and predictive modeling.

5. Financial & Premium Data (Pricing Layer)

This section translates risk into monetary value and premium.

| Data Field | Meaning |

| Total Insured Value (TIV) | Total exposure value |

| Building Value | Value of physical structure |

| Contents Value | Business personal property value |

| Business Income Value | Revenue exposure |

| Rate | Pricing rate applied |

| Base Premium | Initial premium before adjustments |

| Discounts | Credits for favorable risk (e.g., sprinklers) |

| Surcharges | Additional charges for higher risk |

| Final Premium | Total payable premium |

| Minimum Premium | Minimum threshold |

| Deposit Premium | Initial estimated premium |

Implementation Insight:

Premium calculation engines depend on accurate linkage between exposure data and rating factors.

6. Endorsements (Policy Changes Over Time)

Endorsements modify the policy after issuance.

| Data Field | Meaning |

| Endorsement Number | Unique change identifier |

| Endorsement Type | Type of modification |

| Effective Date | When change applies |

| Coverage Change | What changed |

| Limit Change | Increase/decrease in limits |

| Deductible Change | Updated deductible |

| Premium Adjustment | Financial impact |

Implementation Insight:

Endorsements introduce temporal complexity, requiring version-controlled data models.

7. Claims & Loss Data (Post-Loss Intelligence)

Claims data is essential for analytics and AI models.

| Data Field | Meaning |

| Claim Number | Unique claim identifier |

| Date of Loss | When event occurred |

| Cause of Loss | Fire, water damage, etc. |

| Claim Status | Open, Closed |

| Paid Amount | Amount already paid |

| Reserved Amount | Expected future payment |

| Total Incurred | Paid + reserved |

| Loss Location | Where loss occurred |

| Subrogation Indicator | Recovery potential |

Implementation Insight:

Claims data feeds loss models, pricing refinement, and fraud detection systems.

8. Regulatory & Compliance Data

These fields ensure adherence to U.S. insurance regulations.

| Data Field | Meaning |

| State of Issue | Governing jurisdiction |

| Admitted/Non-Admitted | Regulatory classification |

| Form Number | Policy form identifier |

| ISO Form Indicator | Use of standard forms |

9. AI & Advanced Analytics Fields (Derived Layer)

These are engineered features used in machine learning models.

| Data Field | Meaning |

| Risk Score | Composite underwriting score |

| Property Condition Score | Derived from inspections/images |

| Catastrophe Probability | Likelihood of CAT event |

| Expected Loss Cost | Predicted financial loss |

| Fraud Risk Indicator | Likelihood of fraud |

| Image-Based Damage Score | AI-based visual assessment |

| Business Interruption Risk Score | Downtime exposure risk |

Implementation Insight:

These fields are not directly captured but are derived using statistical models, geospatial data, and AI techniques.

How This Data is Used in Systems and AI

1. Core Transaction Systems

- Policy Administration Systems (e.g., Guidewire, Duck Creek)

- Manage policies, coverages, and endorsements

2. Analytical Systems

- Data warehouses and BI tools

- Used for reporting, actuarial analysis, and trend monitoring

3. AI / Machine Learning Systems

- Underwriting automation

- Pricing optimization

- Fraud detection

- Catastrophe modeling

Key Takeaways for Insurtech Projects

- Location-level granularity drives accuracy in underwriting and pricing

- Coverage-to-risk linkage is critical for correct claims handling

- Time dimension (effective dates) must be modeled carefully

- External data (geospatial, weather, ISO) enhances predictive power

- AI models rely on both raw data and engineered features

Conclusion

Commercial property insurance is not just about policies—it is about structured data representing risk, coverage, and financial exposure.

For insurtech professionals, mastering these data fields enables:

- Better system design

- More accurate underwriting models

- Scalable AI-driven insurance solutions

This structured understanding forms the foundation for building modern, data-centric insurance platforms.